No.4095

Medical Imaging Systems Market in Japan: Key Research Findings 2025

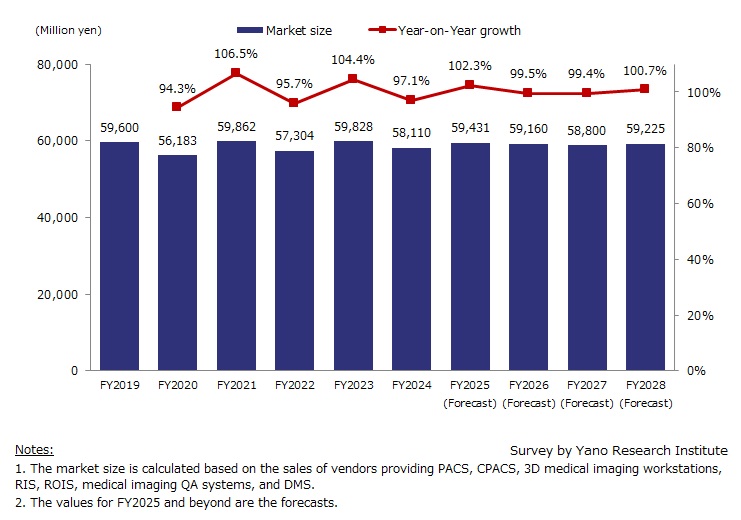

Domestic Medical Imaging Systems Market Declined by 2.9% YoY to 58,110 Million Yen in FY2024

Yano Research Institute (the President, Takashi Mizukoshi) surveyed the domestic medical imaging systems market and found out the market trends by segment, trend of market players, and market outlook.

Market Overview

This survey examines the primary medical imaging systems utilized in hospital settings, including Picture Archive and Communication Systems (PACS), cardiology PACS (CPACS), 3D medical imaging workstations, radiology information systems (RIS), Radiation Oncology Information System (ROIS), medical imaging quality assurance systems, and radiation dose management system (DMS). The market size is calculated based on the sales of business pertaining to these systems.

Market dynamics for core systems are reaching maturity. Market growth for PACS has moderated as the sector shifts from initial installations to a replacement-driven cycle. This same trend is now evident across peripheral systems, such as RIS, ROIS, and imaging QA software.

The demand for dose management systems (DMS) peaked in FY2020, which was driven by the 2020 regulatory mandate for recording patient exposure. However, starting in the latter half of FY2026, the market anticipates a resurgence in activity as systems installed during the 2020 mandate begin their next replacement phase.

Given the circumstances, the domestic medical imaging systems market reached 58,110 million yen in FY2024, representing a 2.9% year-on-year decline (calculated based on the sales of vendors providing these systems). While the market is stabilizing as the impact—and subsequent pullback—of the COVID-19 pandemic wanes, the current valuation reflects a transition toward more cyclical, replacement-based demand.

Noteworthy Topics

AI-Assisted Diagnostic Imaging Systems

While AI-driven solutions have become increasingly prevalent within medical institutions in recent years, their adoption remains largely limited to large hospitals and specialized diagnostic centers. This indicates that widespread market penetration has yet to be achieved. Current market trends are shifting away from simply increasing the number of installations toward establishing robust operational frameworks, including stronger security protocols, precision management, and comprehensive training programs.

To support this transition, the government has launched several strategic initiatives aimed at building centralized medical databases, promoting the secondary use of diagnostic data, and providing subsidies for system implementation. In addition, to facilitate the integration of advanced technologies such as generative AI, the government is actively supporting the development of domestic Large Language Models (LLMs) and has issued formal guidelines for their clinical use. At the same time, the PMDA (Pharmaceuticals and Medical Devices Agency) is working to accelerate its review process, addressing a long-standing bottleneck that has historically delayed the introduction of innovative technologies into the healthcare sector.

The growing need to improve working conditions for medical professionals, coupled with a surge in diagnostic imaging and data volume, has intensified the demand for AI-driven solutions. These tools are increasingly expected to streamline workflows and support diagnostic prioritization. Ongoing R&D focused on reducing clinical workloads and enhancing diagnostic precision is now providing the empirical evidence needed to justify the adoption of AI-powered systems.

However, several complex barriers continue to hinder the widespread adoption of AI-assisted imaging solutions. On the user side, healthcare providers—particularly small-to-medium hospitals and clinics—often struggle to justify the return on investment, as these systems rarely lead to a substantial increase in reimbursable medical fees. Meanwhile, on the supplier side, vendors remain frustrated by the lengthy PMDA approval process.

Future Outlook

Japan’s medical imaging systems market size is projected to stay at around 59 billion yen from FY2025.

Although significant growth is unlikely for the overall market due to the ongoing shift toward replacement-driven demand, industry restructuring continues to progress. Simultaneously, medical imaging system vendors are facing difficulties passing rising costs on to customers despite inflationary pressures. As profitability comes under strain, some suppliers are expected to pursue mergers for survival, while others may withdraw from the market altogether.

Additionally, many medical imaging solution vendors have started developing AI-assisted diagnostic systems. Over the long term, the expansion of services related to AI-assisted diagnostics is expected to reshape the competitive landscape of the medical imaging solutions market.

Research Outline

2.Research Object: Domestic manufacturers of medical imaging systems and devices, and distributors of imported products of such systems

3.Research Methogology: Face-to-face interviews by our expert researchers (including online and email interviews) and secondary research

Medical Imaging Systems Market

In this survey, the medical imaging systems market encompasses Picture Archiving and Communication System (PACS), cardiovascular PACS (CPACS), 3D medical imaging workstations, Radiology Information System (RIS), Radiation Oncology Information System (ROIS), medical imaging quality assurance systems, and radiation dose management system (DMS). The market size is calculated based on the sales of vendors providing these systems.

<Products and Services in the Market>

Radiology PACS, Cardiology PACS, 3D medical imaging workstations, RIS, ROIS, Imaging QA Systems, DMS

Published Report

Contact Us

The copyright and all other rights pertaining to this report belong to Yano Research Institute.

Please contact our PR team when quoting the report contents for the purpose other than media coverage.

Depending on the purpose of using our report, we may ask you to present your sentences for confirmation beforehand.