Domestic Licensed-Brands Retail Market in Japan: Key Research Findings 2016

Research Outline

- Research period: From September to December, 2016

- Research targets: Brand master licensee companies and brand licensee companies

- Research methodologies: Face-to-face interviews by the expert researchers, surveys via telephone/email, and literature research

What is the Domestic Licensed-Brands Retail Market?

The domestic licensed-brands retail market in this research indicates a size of the domestic retail market of fashion brands manufactured and sold through licensing contracts (i.e., contracts to use trademarks) with the overseas or domestic brand producers (the items are listed in Table 1 in this report.) Note that the character brands, including those in the “anime” or animation are not included in this research.

Master licensee companies are defined as those companies that liaise with overseas or domestic brands through direct license contracts. On the other hand, licensee companies are those companies that actually manufacture and sell the licensed-brand products in Japan, under a contract with master licensee companies.

Summary of Research Findings

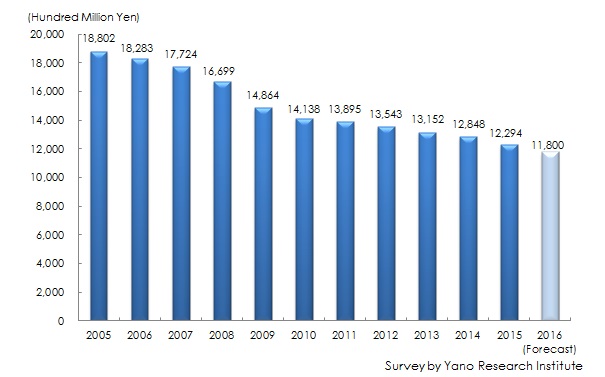

- Domestic Licensed-Brands Retail Market in 2015 Ended Up at 1,229.4 Billion Yen, 95.7% on Y-o-Y Basis, Shrinking Trends Projected to Continue in 2016 to Mark 1,180 Billion Yen, 96.0% of Size in Year Before

The domestic licensed-brands retail market size scaled down in 2015, due to severe environment surrounding the domestic license business largely affected by the stagnant sales at department stores and GMS. This tendency is likely to continue in 2016 where no silver lining yet to be found and plight of the market becoming even fiercer. Therefore, the domestic licensed-brands retail market is projected to be 1,180 billion yen, 96.0% of the size of the previous year.

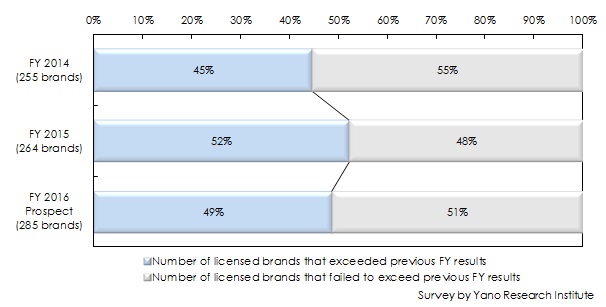

- Though Number of Licensed Brands that Attained Stable Sales Increased in FY2015, Declined Sales Amount at Shrinking or Contract-Ended Brands Overwhelmed Favorable Results

When looking at the trends of individual licensed brands, no matter how sales improved at some of the brands in FY2015 from the previous fiscal year, the domestic licensed-brands retail market size ended up to decline. Diminution of sales from the declining brands (those brands that failed to reach the previous fiscal year results) were so large that it exceeded what earned from the favorable sales of some of the stable brands. What was worse, loss from those contract-ended brands, specifically Burberry, had also brought about significant influence.

- Figure 1: Transition of Size of Domestic Licensed Brands Retail Market

- Figure 2: Composition Ratio between Stable (Favorable) Brands and Failing (Decreasing) Brands