No.4105

Automotive Software (Automakers & Auto Parts Suppliers) Market in Japan: Key Research Findings 2026

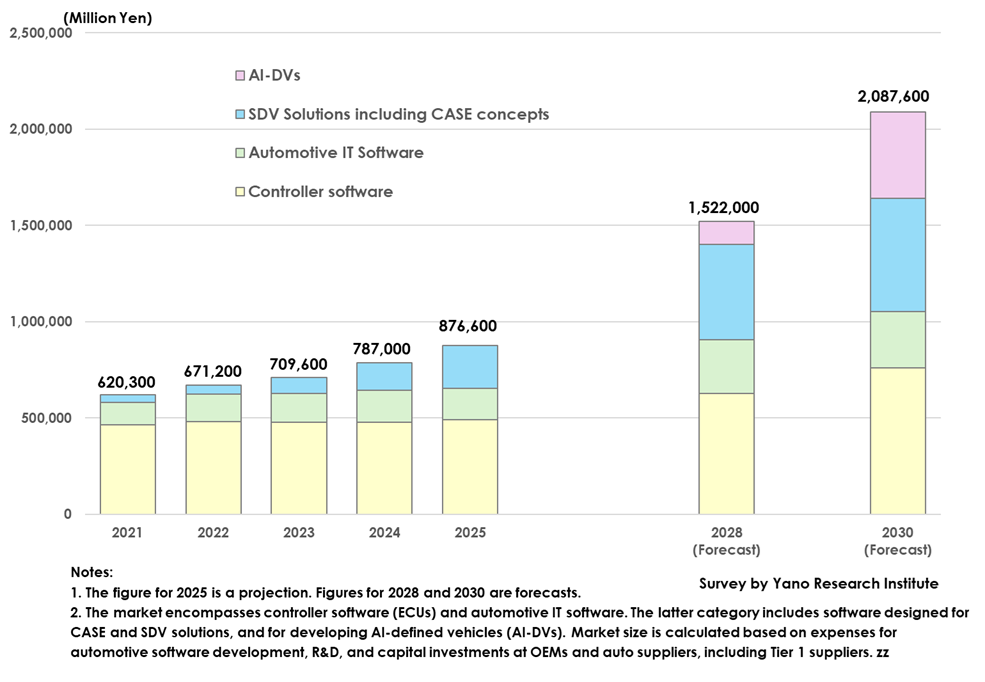

Automotive Software Market Reaches 876.6 billion yen in 2025, Reaching 2 trillion yen by 2030

Yano Research Institute (the President, Takashi Mizukoshi) conducted a survey of the Japanese automotive software market. The survey focused on controller software and automotive IT software developed by original equipment manufacturers (OEMs) and auto parts suppliers. The survey revealed changes in the architecture and development systems of these types of software, as well as the challenges they face and their future directions. Here highlights the market size and composition of controller and automotive IT software, SDV solutions, and AI-defined vehicle (AI-DV) software through 2030.

Market Overview

Automotive software can be broadly classified into two categories: controller software and automotive IT software. While controller software is responsible for the mechanisms that electronically control the automobile, automotive IT software involves the operation of various systems around the driver’s seat. This includes entertainment systems, such as human-machine interfaces (HMIs) and navigation systems, as well as safety systems, including advanced driver-assistance systems (ADAS).

In recent years, software-defined vehicles (SDVs) have garnered attention, surpassing the attention of CASE (connected, autonomous, shared & service, electric) concepts. SDVs were initially just a concept, but they have gained prominence since around 2023 when IT semiconductor manufacturers successively launched software designed and developed for SDVs. This series of software is called SDV solutions. The latest evolution of this trend is AI-defined vehicles (AI-DVs), which utilize AI technologies, such as AI agents and generative AI.

In 2021, the domestic automotive software market reached 620.3 billion yen. Controller software accounted for 74.7% of the market, while automotive IT software accounted for 19.2%, and SDV solutions accounted for 6.1%. By 2023, the market size had grown to 709.6 billion yen, with controller software accounting for 67.5%, automotive IT software accounting for 21.1%, and SDV solutions accounting for 11.4%. These figures indicate a gradual decline in the ratio of controller software and an inverse increase in the ratios of automotive IT software and SDV solutions.

In 2024, the market reached 787.0 billion yen, marking a 10.9% increase from the previous year. Controller software accounted for 60.6% of the market, while automotive IT software and SDV solutions combined accounted for 39.4%. The ratio of controller software has been decreasing since 2022.

The market is projected to reach 876.6 billion yen in 2025, marking an 11.4% year-over-year increase. Controller software is expected to account for 56.2% of the market, while the combined ratio of automotive IT software and SDV solutions is expected to increase rapidly to 43.8%. As some SDV solutions begin to include automotive IT software, the ratio between the two is expected to equalize.

Noteworthy Topics

Mobility Services Will Be Launched Initially for B2B Sector, and B2C Mobility Services Expected to Launch After Level 3 Autonomy

Mobility services are the services generated by obtaining and analyzing vehicle data and information about the vehicle's surroundings from various sensors via over-the-air (OTA) technology. These services are categorized into the B2B and B2C businesses.

Developing mobility services, including application development, requires knowledge of safety and security constraints, including voluntary restraints, established by the Japan Automobile Manufacturers Association (JAMA).

Since many of these constraints aim to reduce automotive accidents, the launch of B2B businesses using data is anticipated. The key to launching these businesses is the use of data owned solely by OEMs.

Meanwhile, B2C businesses for mobility services are not expected to launch until Level 3 autonomous driving, also known as conditional autonomous driving, is realized. In Japan, this launch is expected to include entertainment system applications. Level 3 autonomy enables systems to perform all driving tasks under limited conditions. However, human drivers must immediately resume driving when requested by the system.

Future Outlook

Automotive software development often involves trial and error. Although major domestic OEMs are currently developing vehicle OS, which is operating system installed on a vehicle, as well as peripheral systems at a rapid pace, fruitful results may not be seen until around 2027 or 2028, despite some cases of vehicle OS being installed in some vehicles. As AI agent and Edge AI development is expected to begin around 2026, the market for AI-defined vehicles (AI-DVs) is projected to reach 120.5 billion yen by 2028 and 445.8 billion yen by 2030.

The market for automotive software developed by automakers and suppliers is defined here to comprise controller software, automotive IT software, SDV solutions, and AI-DV software. The increased use of integrated ECUs (mechanisms that use one or a few high-performance ECUs to consolidate control of multiple control units installed on various vehicle parts) causes more automotive IT software to fall under SDV solutions. By 2027, the ratio of automotive IT software to SDV solutions is expected to be approximately 50/50.

While R&D investments in SDVs will stabilize around 2028, investments in AI-DVs will begin around 2026 and rapidly reach 120.5 billion yen by 2028, which is comparable to SDV R&D costs. Consequently, the total market size of controller software, automotive IT software, SDV solutions, and AI-DV software is expected to reach 1.5 trillion yen by 2028, and to reach 2 trillion yen by 2030.

Research Outline

2.Research Object: Automakers, auto parts suppliers (Tier 1, etc.), and automotive software developers

3.Research Methogology: Face-to-face interviews by our expert researchers (including online interviews) and literature research

What is Automotive Software?

Automotive software is broadly classified into two categories: controller software and automotive IT software.

Controller software consists of electronic control units (ECUs) that are responsible for functions such as “go,” “turn,” and “stop,” and the mechanisms that electronically control the automobile. Meanwhile, in this research, automotive IT software is defined as software designed and developed for software-defined vehicles (SDVs) that align with CASE (connected, autonomous, shared & service, electric) concepts.

What is the Automotive Software Market?

For the purpose of this research, the automotive software market encompasses controller software (ECUs) and automotive IT software. The latter category includes software designed for CASE and SDV solutions, and for developing AI-defined vehicles (AI-DVs). Market size is calculated based on expenses for automotive software development, R&D, and capital investments at OEMs and auto suppliers, including Tier 1 suppliers.

Published Report

Contact Us

The copyright and all other rights pertaining to this report belong to Yano Research Institute.

Please contact our PR team when quoting the report contents for the purpose other than media coverage.

Depending on the purpose of using our report, we may ask you to present your sentences for confirmation beforehand.