No.3878

Automotive Software (Developed by Software Development Vendors, IT Semiconductor Vendors, and Microcontroller Vendors) in Japan: Key Research Findings 2025

The Market of Domestic Automotive Software (Developed by Software Development Vendors, IT Semiconductor Vendors, and Microcontroller Vendors) Projected to Attain 679 Billion Yen in 2025, Forecasted to Reach 1,011.8 Billion Yen By 2030

Yano Research Institute (the President, Takashi Mizukoshi) has conducted a survey on the domestic automotive software market, and found out the trends of controller software, automotive IT software, and SDV solutions developed by subcontractors (software vendor, IT semiconductor manufacturer, and microcontroller vendor). The market report highlights transition and challenges in architecture and development environments, and future directions.

This press release denotes our forecast on the market size and market composition of automotive software by 2030 (controller software, automotive IT software, and SDV solutions).

Market Overview

Automotive software has been categorized briefly into controller software and automotive IT software. Controller software are small computers inside ECUs (CPU), each of which electronically controls specific system, such as system for “run,” “turn,” and “stop”, respectively. On the other hand, automotive IT software refers to a system for various systems using a Human-Machine Interface (HMI) often displayed on a car's dashboard, including infotainment with a focus on navigation system and driver assistance system (ADAS).

Today, Software-Defined Vehicle (SDV), a new concept, is gaining momentum in the automotive industry. As seen in a number of software for SDV (SDV solutions) being launched in the market one after another since around 2023 by IT semiconductor manufacturers, SDV is increasing presence rapidly.

In this research, the automotive software market encompasses controller software and automotive IT software, as well as SDV solutions. The market size is calculated based on the price of automotive software developed by subcontractors of automotive OEMs and auto parts suppliers (Tier 1 and Tier 2), including automotive software vendors, IT semiconductor vendors, and microcontroller vendors.

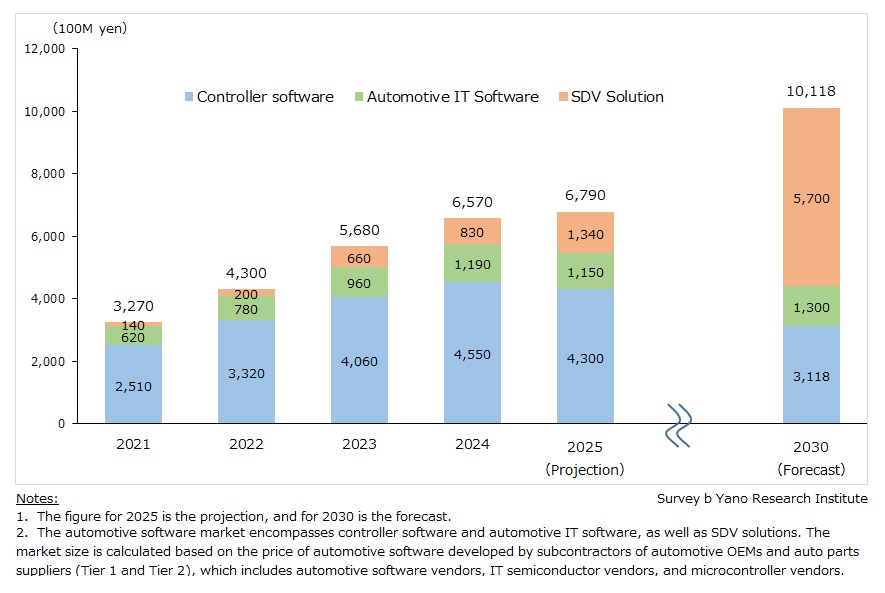

It is estimated that the automotive software market amounted to 430 billion yen in 2022 (131.5% of the previous year), 568 billion yen in 2023 (132.1% on the same basis), and 657 billion yen in 2024 (115.7% on the same basis), indicating a steady growth trend over the period.

In 2024, the market composition was as follows: controller software, 69.3%; automotive IT software, 18.1%; and SDV solutions, 12.6%.

Noteworthy Topics

Concept of SDV Potentially Commoditizes Controller Software and Diminishes Presence of Conventional Software Development Vendors

In the past, most conventional software vendors positioned themselves between microcontroller vendors (that manufacture controller software) and automotive OEMs and auto parts suppliers (Tier 1, Tier 2), providing solutions closely aligned with OEM needs. Looking ahead, however, the automotive software market is expected to see gradual technological convergence between 2024 and 2028, with automotive IT software shifting toward SDV-oriented solutions developed by IT semiconductor and microcontroller vendors. At the same time, the rise of the SDV concept is making controller software increasingly commoditized, reducing differences among controller software, and potentially leading to its eventual integration into SDV platforms.

Given this situation, there is a strong likelihood that OEMs will shift their strategies toward SDVs. In automotive software, development approaches are expected to move away from the traditional vertical integrated, OEM-led model toward horizontal specialization. As a result, the role of software development vendors that once occupied niche positions is likely to diminish. Some leading software development vendors with strong sense of risks are already taking measures to secure their survival.

Future Outlook

The market size of automotive software in 2025 (as a total of automotive software developed by software development vendors, IT semiconductor vendors, and microcontroller vendors) is expected to reach 679 billion yen. By market composition, SDV solutions will exceed automotive IT software (19.7% and 16.9%, respectively). SDV solutions are projected to surge by 61.4% year-on-year while automotive IT software will decrease by 3.4% on same basis, against the backdrop of the convergence, due to a shift in demand for automotive IT software shifting toward SDV-oriented solutions mainly developed by IT semiconductor and microcontroller vendors.

Going forward, OEMs are expected to further accelerate software development related to SDVs, including the development of SoCs (System-on-a-Chip). Software development vendors, IT semiconductor manufacturers, and microcontroller vendors are all projected to continue steady growth. The automotive software market (developed by software development vendors, IT semiconductor manufacturers, and microcontroller vendors) is forecasted to reach 1,011.8 billion yen by 2030. SDV solutions are expected to account for 56.3% of the market, making them the largest segment.

Research Outline

2.Research Object: Vendors developing automotive software (software development vendors, IT semiconductor vendors, and microcontroller vendors)

3.Research Methogology: Face-to-face interviews by our expert researchers (including online interviews) and literature research

<What is Automotive Software? >

Automotive software has been categorized briefly into controller software and automotive IT software. Controller software are small computers inside ECUs (CPU), each of which electronically controls specific system, such as system for “run,” “turn,” and “stop”, respectively. On the other hand, automotive IT software refers to a system for various systems using a Human-Machine Interface (HMI) often displayed on a car's dashboard, including infotainment with a focus on navigation system and driver assistance system (ADAS).

Today, Software-Defined Vehicle (SDV), a new concept, is gaining momentum in the automotive industry. As seen in a number of software for SDV (SDV solutions) being launched in the market one after another since around 2023 by IT semiconductor manufacturers, SDV is increasing presence rapidly.

* Electronic Control Unit (ECU): Controllers inside the vehicle, each of which electronically controls a single system like lane keeping system, distance control system, etc. The proliferation of electronics has increased the number of ECUs in a vehicle, creating issues such as negative impact on vehicle performance due to combined weight of ECUs and rising costs.

<What is the Automotive Software Market?>

In this research, the automotive software market encompasses controller software and automotive IT software, as well as SDV solutions.

Considering that automakers (OEMs) have started developing System-on-a-Chip (SoC), we have included IT semiconductor manufacturers and microcontroller vendors as our research targets. The market size is calculated based on the price of automotive software developed by subcontractors of automotive OEMs and auto parts suppliers (Tier 1 and Tier 2), including automotive software vendors, IT semiconductor vendors, and microcontroller vendors.

Note that the market size does not include software development cost, R&D expenses and capital expenditure at automotive OEMs and auto parts suppliers.

<Products and Services in the Market>

Automotive software developed in Japan by subcontractors (software development vendors, IT semiconductor vendors, and microcontroller vendors)

Published Report

Contact Us

The copyright and all other rights pertaining to this report belong to Yano Research Institute.

Please contact our PR team when quoting the report contents for the purpose other than media coverage.

Depending on the purpose of using our report, we may ask you to present your sentences for confirmation beforehand.