No.3726

Eight Major Construction Segments in Japan: Key Research Findings 2025

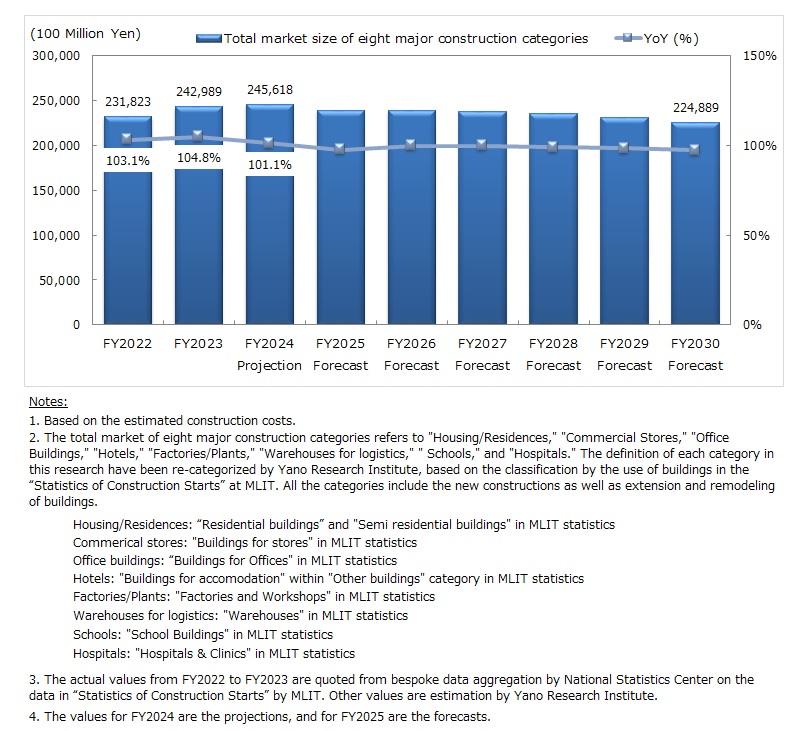

Market Size for Eight Major Construction Segments in Japan Valued at 24,298,900 Million Yen for FY2023, Representing 104.8% of Previous Fiscal Year

Yano Research Institute (the President, Takashi Mizukoshi) carried out a survey on the eight key construction segments in Japan, and found out the market size, trends by segment, and future perspective.

Market Overview

The eight major construction segments (residential, offices, retail, hospitality, industrial, logistics, education, and healthcare) for FY2023 increased to 24,298,900 million yen, based on the planned construction costs (representing 104.8% of the previous fiscal year).

Driven by the resumption of construction projects that were delayed during the COVID-19 crisis alongside a recovery of overall construction demand, the market for eight major construction segments showed an upward trend. Growth is fueled particularly by strong demand in logistics and industrial segments.

However, construction cost has been soaring from around 2021 due to the increase in material price and labor expenses. To manage the rise in cost, contractors reduced the planned floor sizes of buildings, or postponed/canceled the projects.

Noteworthy Topics

Adapting to Surging Construction Costs

Construction costs have been surging since around 2021, due to soaring labor expenses and material prices. The increase in labor cost is largely due to supply-demand imbalance in the construction workforce. This issue stems from a decline in the number of jobseekers in the industry, leading to an aging workforce and a shrinking overall labor pool. Meanwhile, the rise in material costs is primarily attributes to what's been dubbed as the 'Wood Shock' *1 and 'Iron Shock.'*2

*1 ‘Wood Shock’ refers to a global surge in lumber prices, driven by a spike in new housing construction following the pandemic, particularly in China and the U.S. This surge caused a sharp increase in lumber price.

*2 ‘Iron Shock’ describes the rise in iron and steel prices, fueled by a rapid global increase in demand for these markets in the wake of the COVID-19 crisis.

Future Outlook

The market size for eight major construction segments (residential, offices, retail, hospitality, industrial, logistics, education, and healthcare) for FY2024 based on the planned construction cost is expected to expand to 24,561,800 million yen (representing 101.1% of the preceding fiscal year) due to higher construction expenses associated with rising commodity prices.

On the supply side, strong demand persists for large-scale renovations of office buildings and commercial facilities in central Tokyo, as well as for warehouses and semiconductor foundries, supporting steady growth in these segments.

In contrast, overall demand is expected to decline due to population shrinkage, downsizing of buildings driven by rising construction costs, and delays in project starts caused by those same cost pressures. As a result, the combined market size of the eight major construction segments is projected to fall to 22,488,900 million yen by FY2030 (92.6% of that of FY2023 level).

Research Outline

2.Research Object: Eight key construction segments (Residential, Offices, Retail, Hospitality, Industrial, Logistics, Education, and Healthcare)

3.Research Methogology: Information gathered from documents and publicly available data, analysis based on custom data aggregation conducted by the National Statistics Center using data from the Statistics of Construction Starts compiled by the Ministry of Land, Infrastructure, Transport and Tourism (MLIT).

Eight Major Construction Segments

In this research, eight major construction segments refer to the following sectors: residential, offices, retail, hospitality, industrial, logistics, education, and healthcare. The definition of each segment is based on the “classification by the usage of buildings” in the Statistics of Construction Starts by the Ministry of Land, Infrastructure, Transport and Tourism (MLIT). All segments encompass new construction as well as building extensions and renovations.

The market size is calculated based on planned construction costs. Actual figures through FY2023 drawn from bespoke data aggregated by National Statistics Center, based on the Statistics of Construction Starts published by MLIT. Other figures are forecasts by Yano Research Institute.

<Products and Services in the Market>

Housing (e.g. single-family homes, multifamily housing, apartments, condos), offices, retail stores, hotels, factories, warehouses, schools, hospitals

Published Report

Contact Us

The copyright and all other rights pertaining to this report belong to Yano Research Institute.

Please contact our PR team when quoting the report contents for the purpose other than media coverage.

Depending on the purpose of using our report, we may ask you to present your sentences for confirmation beforehand.