No.3172

Mobile Communications (Services & Terminals) Market in Japan: Key Research Findings 2022

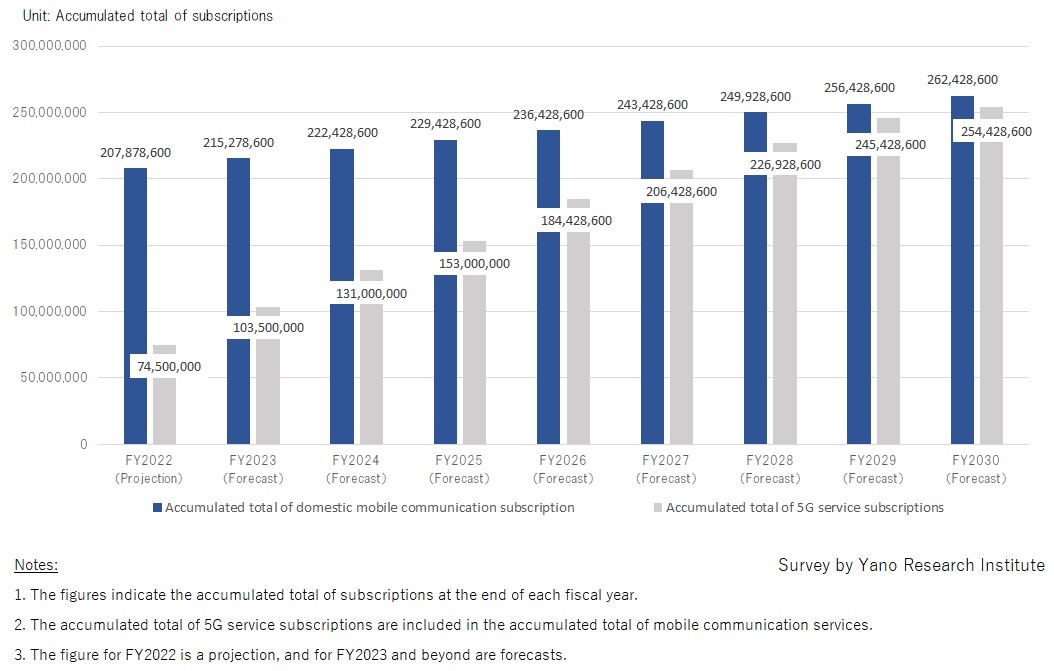

Domestic 5G Subscription Projected to Reach 74.5 Million for FY2022 (Accumulated Total, Year Ending March 31, 2023)

Yano Research Institute (the President, Takashi Mizukoshi) has carried out a survey on the domestic mobile communication market (services and terminals), and this press release announces the forecast up to FY2030.

Market Overview

Adopted widely, the domestic mobile phone service has become social infrastructure. Whilst the current mobile phone services are mostly based on a fourth-generation (4G) LTE standards, carriers are transitioning to a fifth-generation (5G) standard, which offers high-speed, large-capacity, and stable connection. At the same time, while the third-generation (3G) standard expects termination, market entry of “mobile virtual network operators (MVNO)” has prompted users of feature phones to switch to smartphones further. In addition to the fact that social media, mobile payment apps, and music/video streaming services on mobile phones has been entrenched in our everyday lives, when the linkage to My Number Card is enhanced, smartphones increase importance more than ever.

Noteworthy Topics

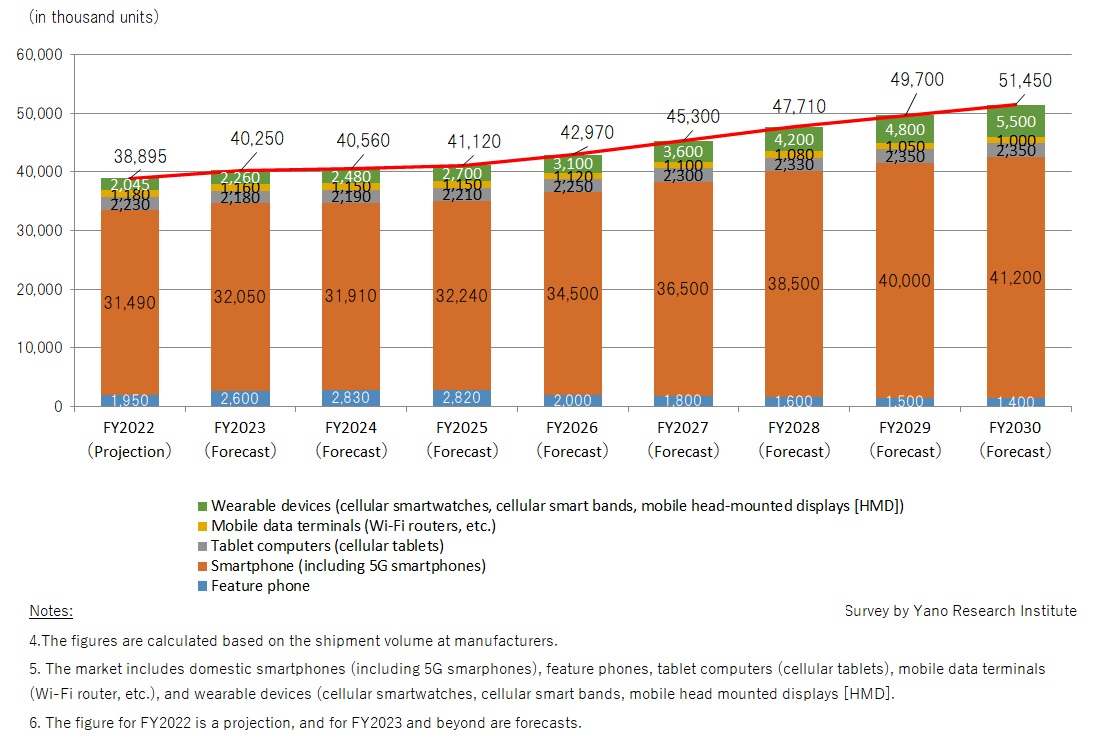

Trends of Domestic Mobile Terminal Market

Shipment volume of domestic mobile terminals for FY2022 (accounting year ending March 31, 2023) is projected to reach 38,895,000 units. By product category, this breaks down into 31,490,000 smartphones, 2,230,000 cellular tablets, 1,180,000 mobile data terminals (Wi-Fi routers etc.), 1,950,000 feature phones, and 2,045,000 wearable devices (cellular smartwatches, cellular smart bands, mobile head-mounted display [HMF]).

Drop in shipment is anticipated particularly for smartphones, as a repercussion to the increased demand during the COVID crisis and the price rise due to weak yen. Nor can it expect significant growth in a medium- to long-term, against the backdrop of the price rise due to appreciation of yen and the demand shrinkage. On the other hand, driven by the rise of health consciousness and increase of manufacturers making market entrance, the shipment volume of wearable devices, especially smartwatches, is forecasted to augment.

Future Outlook

An accumulated total of domestic mobile communication service subscription is projected to reach 207,878,600 for FY2022 (the year ending March 31, 2023), of which 74,500,000 are subscribed to 5G service. Along with the expansion of 5G coverage, standalone (SA) service* will be introduced, which is expected to promote a rise of services that utilize advantages of 5G, which is high-speed, large-capacity, and low latency. Moreover, as penetration-price smartphones began to adapt to 5G, users are expected to subscribe to unlimited data plan for their 5G smartphones at the time of their replacement.

Considering that SoftBank plans to terminate its 3G service in January 2024, replacement demand is most likely to multiply the smartphone subscription for FY2023. In a medium-term, the replacement demand can be expected up to March 2026, which is the timing that NTT Docomo terminates their 3G service. Furthermore, since introduction of “5G Evolution”, which refers to the advanced 5G (5.5th generation standard), is anticipated to start from FY2026, new services that utilizes 5G’s characteristics, the high speed, high capacity, and low-latency. There is a high expectation for mobile communication for IoT, especially for automotive connected services and utilization of Metaverse. The accumulated total of domestic mobile communication service subscription is forecasted to reach 262,428,600 by FY2030 (the accounting year that ends on March 31, 2031), which includes 25,442,8600 subscription of 5G service.

* Unlike non-standalone (NSA) service that offers 5G service using 4G network infrastructure, standalone (SA) service refers to the service provided with infrastructure dedicated to 5G (base station, core network). SA service has more advantages in making use of 5G’s characteristics, the “high speed/high capacity,” “ultra-low-latency”, and “massive device connectivity”.

Research Outline

2.Research Object: Domestic mobile network operator, manufacturers of mobile terminals and parts, distributors, etc.

3.Research Methogology: Face-to-face interviews by our expert researchers (including online interviews), interview at seminars, and literature research.

What is the Domestic Mobile Communication (Services & Terminals) Market?

In this research, the term mobile communication service is used as a generic term for voice call and data transmission services provided by mobile network operators. At current, the mobile communication services are mainly a fourth-generation (4G) LTE standard. Commercial deployment of the fifth generation (5G) standard started in April 2020. The domestic mobile communication terminals market refers to smartphones (including 5G phones), feature phones, tablet (cellular tablets), mobile data terminals (Wi-Fi routers etc.), and wearable devices (cellular smartwatches, cellular smart bands, mobile head-mounted displays [HMF]). The market size is calculated based on the shipment volume at manufacturers. Figures for the accumulated total of domestic mobile communication service subscriptions, and the shipment volume of domestic mobile terminals by category, are both calculated for a fiscal year (starting April 1 and ending March 31 of the following year).

<Products and Services in the Market>

Mobile communication services (voice calls, data transmission), smartphones, feature phones, tablets, wearable devices (smartwatch, smart band, HMD, etc.)

Published Report

Contact Us

The copyright and all other rights pertaining to this report belong to Yano Research Institute.

Please contact our PR team when quoting the report contents for the purpose other than media coverage.

Depending on the purpose of using our report, we may ask you to present your sentences for confirmation beforehand.