No.3313

Carbon Neutrality Efforts by Chemical Industry in Japan: Key Research Findings 2023

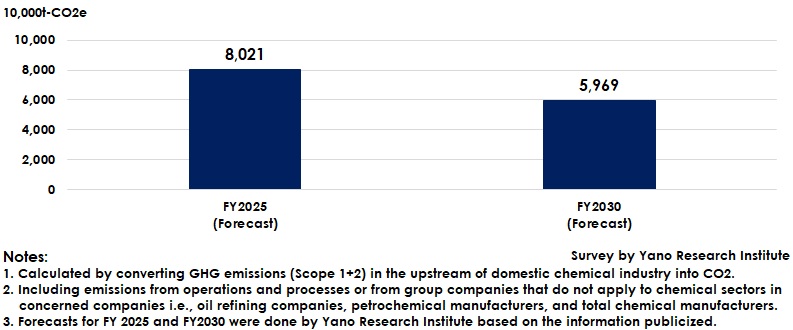

FY2030 Projection of GHG Emissions (Scope 1+2) in Upstream of Domestic Chemical Industry to be 59,690 Thousand Ton-CO2e

Yano Research Institute (the President, Takashi Mizukoshi) carried out a survey on the carbon neutrality efforts in chemical industry and found out the trends at oil refining companies, petrochemical manufacturers, comprehensive chemical manufacturers, status and challenges in carbon neutral technology, and future perspectives.

Market Overview

Among domestic industrial sectors, chemical industry is positioned as the industry with high CO2 emissions following steel. To achieve decarbonization as a nation, it is indispensable to attain carbon neutrality in chemical industry.

The supply chain in chemical industry stretches out from its origin, i.e., naphtha, a petroleum product that goes through various processes and businesses to final products, making further the downstream, wider range of companies and industries widespread. Therefore, if carbon neutrality is achieved at companies in the upstream of supply chain where basic petrochemicals that are raw materials of chemical products such as plastic, synthetic rubber, fiber, etc. are manufactured, it will bring about enormous influence.

When observing CO2 emission sources at each upstream-positioned company by Scope, main emissions that apply to Scope 1 and 2, i.e., company-level emissions, are fuel-consuming facilities such as coal-used thermal power generation facilities and naphtha cracking furnaces. For the sources of Scope 3, on the other hand, that falls into entire supply-chain-wide emissions, are occupied mostly by the products bought. Companies have started propelling 1) fuel switching for Scope 1 and 2, 2) resource circulation and collection (CCUS: Carbon dioxide capture, utilization, and storage) for Scope 1 to 3, 3) chemical recycling (see below) and 4) raw material switching for Scope 3.

Noteworthy Topics

Efforts to Tackle Scope 3 at Upstream of Domestic Chemical Industry

Companies positioned at the upstream of chemical industry have set the target reduction rates of CO2 emissions for Scope 1 and 2 toward 2030 as the mid-term goal, in addition to the carbon neutrality target by 2050. Currently, each company mainly makes efforts to reduce carbon emissions for Scope 1 and 2 by switching fuels of or increasing the energy efficiency of coal-used thermal power generation facilities and naphtha cracking furnaces.

Meanwhile, most companies do not understand the entire supply-chain-wide emissions to respond to Scope 3 issue, due to complication of the supply chain. While some companies investigate, calculate, and compile CO2 emissions for Scope 3, some make efforts by technological development for contributing to reduction of Scope 3 CO2 emissions in the upstream of chemical industry. To be specific, carbon dioxide capture and utilization (CCU), carbon dioxide capture and storage (CCS), both of which also contribute to Scope 1 and 2, and chemical recycling in which waste plastics and waste materials are chemically treated and returned to raw materials before being reused.

In addition, to reduce Scope 3 emissions, there are moves by those companies in the upstream of chemical industry to consider procuring or shifting to bio naphtha, byproduct of SAF (Sustainable Aviation Fuels), from the conventional petroleum-derived naphtha.

Future Outlook

While development of technologies for chemical recycling and CCU/CCS are underway in chemical industry, such technologies, in most cases, are not in the phase of implementation. Companies are making efforts, to the extent of what they can, to reduce emissions for Scope 1 and 2.

Reduction of CO2 emissions for Scope 3, however, is the urgent matter to be solved for realization of carbon neutrality. In particular, chemical recycling is regarded as the key. Though material recycling, that is the reuse of one object from another, is the mainstream recycling in entire chemical industry, the conditions of the waste to be processed and the range of reusable applications are limited. To shift from the current material recycling to chemical recycling, it is necessary for each company in the upstream of the industry to swiftly make decisions on the investment to achieve early implementation of chemical recycling. Nevertheless, chemical recycling is not necessarily omnipotent under every condition, so that it is required to use material recycling accordingly when suitable.

After FY2025, as the upstream of chemical industry expects increase in the co-firing ratio of low-carbon fuels, deployment of decarbonized fuels, implementation of CCUS, and operation of chemical recycling plants, the GHG emissions (Scope 1+2) in the upstream of the industry is projected to be 59,690 thousand ton-CO2e by FY2030.

Research Outline

2.Research Object: Oil refining companies, petrochemical manufacturers, comprehensive chemical manufacturers

3.Research Methogology: Face-to-face interviews (online included) by our specialized researchers, and literature research

About Chemical Industry

The chemical industry in this research targets those companies in the upstream of supply chain, centered on oil refining companies, petrochemical manufacturers, and comprehensive chemical manufacturers.

To calculate greenhouse gas (GHG) emissions in the upstream of the domestic chemical industry, the research gives the forecast value on the emissions by FY2025 and FY2030, targeting Scope 1 and 2 of in-house emissions at businesses.

The GHG emission calculation is based on the followings:

Scope 1: Direct emission of GHG by the businesses themselves (combustion of fuels, industrial processes)

Scope 2: Indirect emission that associates with the use of electricity, heat/steam that are supplied by other companies.

Scope 3: Indirect emissions that do not apply to Scope 1 or 2 (Emissions that involves business activity by the company but emitted by another company)

Reference: Ministry of the Environment Website

https://www.env.go.jp/earth/ondanka/supply_chain/gvc/en/

<Products and Services in the Market>

Raw material switching, fuel switching, resource circulation, chemical recycling, hydrogen/ammonia fuels, biomass fuel, CCUS (CCU/CCS)

Published Report

Contact Us

The copyright and all other rights pertaining to this report belong to Yano Research Institute.

Please contact our PR team when quoting the report contents for the purpose other than media coverage.

Depending on the purpose of using our report, we may ask you to present your sentences for confirmation beforehand.