No.3454

Automotive Software (Developers) Market in Japan: Key Research Findings 2023

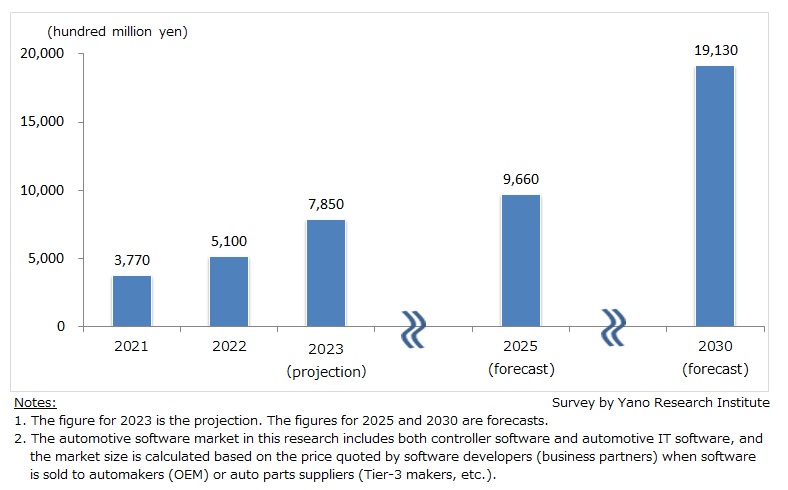

Domestic Automotive Software (Developers) Market Size Estimated at 785 Billion Yen in 2023, Forecasted to Reach 1,913 Billion Yen by 2030

Yano Research Institute (the President, Takashi Mizukoshi) has conducted a survey on the automotive software (developers) market in Japan, and found out the trends of automotive software (controller software and automotive IT software) from software developers’ perspective, the changes in development formation, challenges, and future directions. This press release announces our forecasts on transition of the automotive software market size to 2030 and the ratio of controller software to automotive IT software.

Market Overview

We have categorized automotive software briefly into controller software and automotive IT software.

Controller software is the electric controller for automobile, the ECU*1 units, which is increasing in line with advancements of ADAS (Advanced driver-assistance system) technology. Automotive IT software is the software developed in alignment to CASE (Connected、Autonomous、Shared & Service、Electric), which is cloud-based platform for various applications including infotainment apps.

The market size of automotive software, including both controller software and automotive IT software, is estimated at 377 billion yen in 2021, 510 billion yen in 2022 (135.3% YoY), and 785 billion yen in 2023 (153.9% YoY), based on the price quoted by software developers when software is sold to automakers (OEM) or auto parts suppliers (such as Tier-1 makers).

A ratio of controller software to automotive IT software in 2021 is estimated at 70.3% to 29.7%.

*1 ECUs (Electronic Control Units) are on-board computers that electrically controls the vehicle, such as to stay in a lane, keep distance from the car ahead, etc. As component count per vehicle increases, reducing total weight and costs of ECUs has become a challenge of the industry.

Noteworthy Topics

Automotive Software for Realization of SDV

To realize SDV *2, automakers (OEMs), auto parts suppliers (Tear-1, etc.), and partner companies (software developers) are engaged in research and development of automotive software, especially those that align with the concept of CASE. While control software is optimized individually for a particular purpose, automotive IT software is characterized by system design approach from total optimization perspective. Examples of automotive IT software include systems compliant with standards like AUTOSAR Adaptive Platform and automotive operating systems, which is software platform. The architecture of SDV will include on-board controller software and automotive IT software.

However, in light of challenges to reduce total weight and costs, the number of former software is destined to narrow down by the development of integrated ECU, except for critical ECUs (that requires real-time processing).

Meanwhile, automotive IT software will be a platform for various automotive-related applications.

In view of the automotive IT software component by layer, layer 1, the basic infrastructure, is HPC*3. Layer 2 is componentized by systems compliant with standards such as AUTOSTAR Adaptive Platform. Then, on layer 3, multiple on-board applications including entertainment apps are expected to be developed via cloud environment using API (Application Programming Interface) of automotive OS, while an update to an embedded software and application will be delivered through a wireless network (Over-The-Air update).

*2 SDV (Software Defined Vehicle) refers to any vehicle that adds functionality and enables new features through automotive software.

*3 HPC (High Performance Computing) software delivers accelerated computing for complex calculations and processing data at high speeds.

Future Outlook

Size of the automotive software (developer) market is forecasted to reach 966 billion yen by 2025. It is assumed that, as OEMs and auto parts suppliers increasingly consign R&D of automotive IT software to software developers, the ratio of automotive IT software in the market will outstrip the ratio of controller software.

Assuming that actual installation of the new technologies will be available around 2030, we believe the market size of automotive software will reach 1,913 billion yen by 2030. By then, the composition ratio of controller software and automotive IT software is expected to reverse.

Research Outline

2.Research Object: Automotive software developers

3.Research Methogology: Face-to-face interviews by our expert researchers (including online interviews) and literature research

<What is the Automotive Software? >

Automotive software can be categorized briefly into 1) controller software and 2) automotive IT software.

Controller software refers to controllers, the ECU units (CPU) that electronically control automobile that are dedicated to a single function, such as run, turn, and stop. On the other hand, we define software with design and development aligned to CASE (Connected、Autonomous、Shared & Service、Electric) and SDV as automotive IT software (infotainment software and driver assistance systems, etc.).

<What is the Automotive Software Market?>

The automotive software market in this research includes both controller software and automotive IT software, and the market size is calculated based on the price quoted by software developers (business partners) when software are sold to automakers (OEM) or auto parts suppliers (Tier-1 makers, etc.).

However, the market size does not include the price of automotive software developed by OEM and auto parts suppliers, nor R&D expenses and capital expenditure at these companies.

<Products and Services in the Market>

Domestic automotive software developed by software developers

Published Report

Contact Us

The copyright and all other rights pertaining to this report belong to Yano Research Institute.

Please contact our PR team when quoting the report contents for the purpose other than media coverage.

Depending on the purpose of using our report, we may ask you to present your sentences for confirmation beforehand.